PA

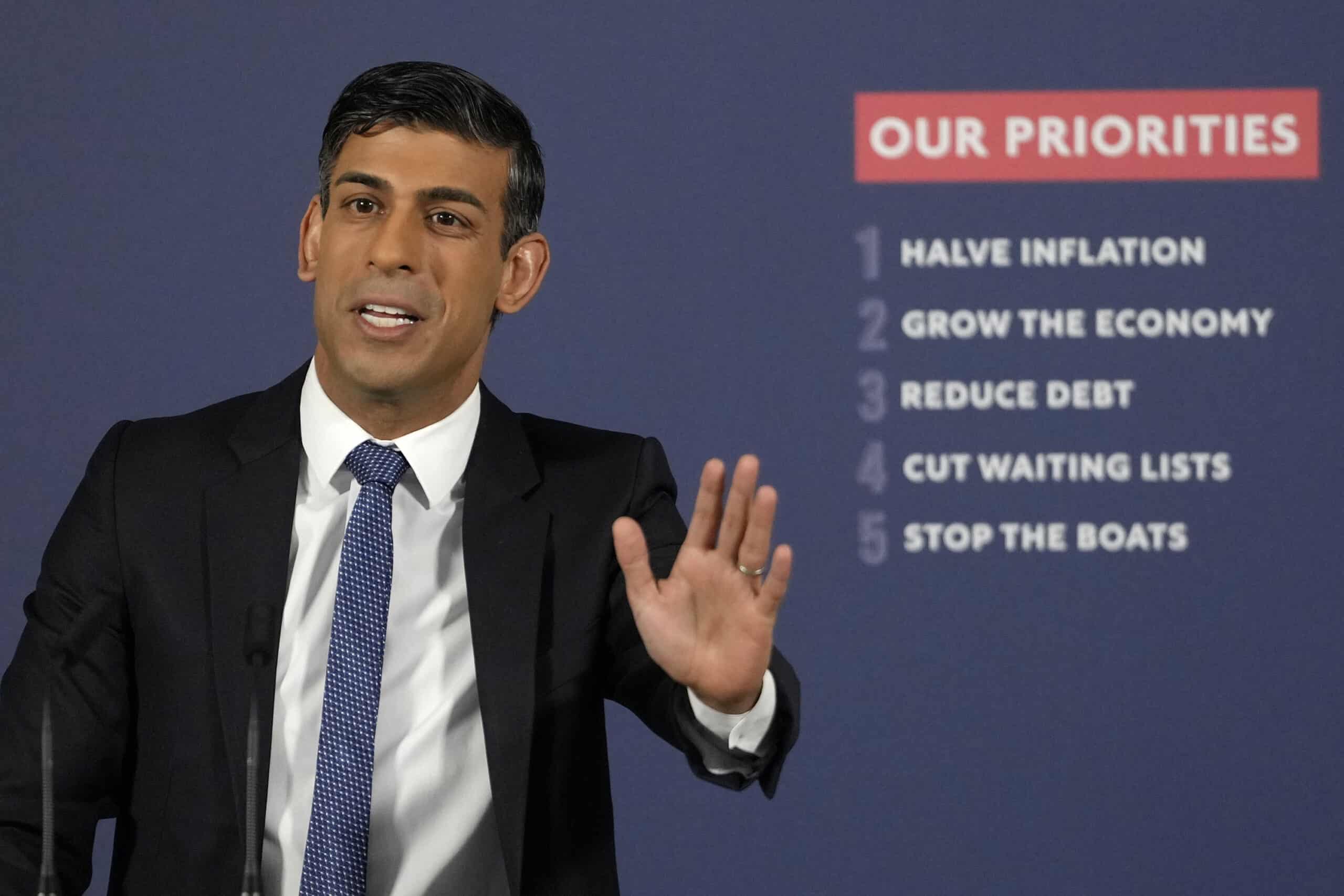

The Conservative’s five priorities ahead of the next general election look to already be in tatters as another key pledge bites the dust.

Rishi Sunak promised to stop the boats ahead of the big day in 2024 as well as halve inflation, grow the economy and cut waiting lists.

But most of the promises are already unraveling.

Today it was revealed another key pledge – to reduce government debt – looks to be set to fail.

The rocketing cost of energy bills support and soaring debt interest saw UK government borrowing jump by more than £18 billion in the year to March, according to official figures.

The Office for National Statistics (ONS) said the public sector borrowed £139.2 billion in the past financial year – the fourth highest since records began and £18.1 billion more than in 2021-22, according to official figures.

But the figure was lower than the £152.4 billion predicted last month by Britain’s fiscal watchdog, the Office for Budget Responsibility (OBR).

This comes despite the Government forking out £41.2 billion over the past six months to support households and businesses with energy costs.

Sky-high inflation also pushed debt interest payments on public sector debt to £106.6 billion – 47 per cent higher than the previous year as painful rises in Retail Prices Index inflation have increased the interest payable on index-linked gilts.

Chancellor Jeremy Hunt said the Government was right to spend on energy support in the cost-of-living crisis, but warned “we cannot borrow forever”.

Related: Watchdog extends investigation into PM’s declaration of interests